Poland’s Financial Mainstream Still Thinks Finance Means Banks

A small audit of the European Financial Congress agenda shows how little space Poland’s financial establishment gives to cryptoassets, stablecoins and tokenised finance.

Poland has one of the most technologically advanced banking sectors in Europe. Mobile banking is good, instant payments are widely used, and BLIK has become one of the country’s best-known payment innovations. This is a genuine achievement.

But success creates blind spots.

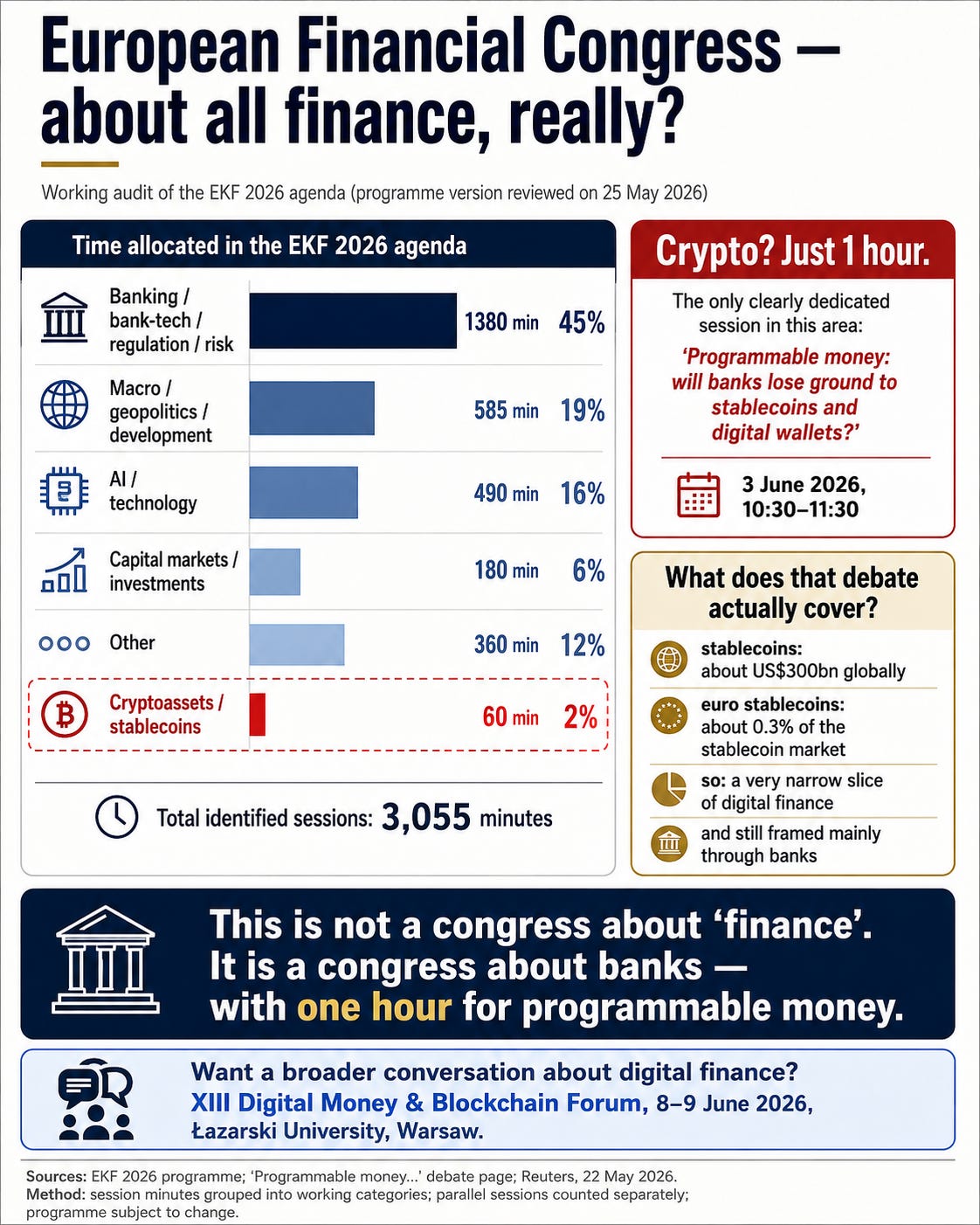

The 2026 European Financial Congress, one of Poland’s most important annual gatherings of bankers, regulators, consultants and financial-sector executives, is a useful case study. I reviewed its programme not by looking at personalities, sponsors or institutional politics, but by asking a simpler question: how much time does the agenda allocate to different parts of the financial system?

The answer is revealing. The European Financial Congress is, in practice, much more a banking and regulatory congress than a congress about finance as a whole.

The audit

My method was deliberately simple. I classified sessions in the publicly available EKF 2026 programme into broad categories and counted the number of minutes allocated to each. Parallel sessions were counted separately because the purpose was not to reconstruct a participant’s possible individual path through the event, but to measure the weight assigned to each topic by the programme itself.

This is not a perfect scientific classification. Some panels naturally overlap across categories: AI in banks, regulatory risk, macroeconomic security, capital markets, public policy. But even with this caveat, the structure of the programme is clear.

In my working classification, broadly defined banking topics — banking, bank-tech, regulation, legal and operational risk, bank business models and financial-sector resilience — account for roughly 45% of the identified session time.

Cryptoassets and stablecoins account for about 60 minutes, or less than 2% of the programme.

That would already be notable. What makes it more interesting is the framing of that one session.

The only clearly visible session in this area is titled:

“Programmable money: will banks lose ground to stablecoins and digital wallets?”

The question is not: how is the architecture of finance changing? It is not: what does tokenisation mean for capital markets, payments, custody, supervision or monetary sovereignty? It is not: how should Poland position itself in the emerging on-chain financial infrastructure?

The question is: will banks lose ground?

That framing matters.

This is not really a session about crypto

The EKF session is not about the full cryptoasset market. It is not about Bitcoin, Ethereum, DeFi, tokenised financial instruments, on-chain settlement, custody infrastructure, cryptoasset service providers under MiCA, market abuse, exchange supervision, wallet infrastructure, or the changing structure of digital capital markets.

It is mainly about programmable money, tokenised deposits, CBDCs and euro stablecoins — and even there, the central perspective is the banking sector.

This is not irrelevant. On the contrary, stablecoins, tokenised deposits and CBDCs are important topics. But they represent only a narrow part of the broader digital-asset ecosystem. A conference that devotes one hour to this topic, and frames it mostly through the question of whether banks can preserve their position, is not really mapping the future of finance. It is mapping how incumbent institutions perceive a threat.

This is the distinction that matters.

The numbers are not large enough to justify hype, but they are large enough to justify attention

Cryptoassets are not larger than banks, insurers or investment funds. They do not yet dominate the financial system. They are volatile, unevenly regulated, technically complex and still associated with major fraud, operational failures and speculative excess.

But they are not marginal either.

At the time of writing, the global cryptoasset market capitalisation is around USD 2.6 trillion. Stablecoins alone account for more than USD 300 billion. Euro-denominated stablecoins remain tiny — roughly 0.3% of the global stablecoin market — but this is precisely why the topic is strategically important for Europe.

The issue is not only current size. The issue is infrastructure.

Stablecoins are not just another speculative token category. They are used as settlement assets in crypto markets, as liquidity instruments, as payment rails, and increasingly as a bridge between traditional finance and blockchain-based systems. Tokenised deposits, e-money tokens and CBDCs are different institutional answers to the same underlying question: who will issue, control and settle digital money in programmable financial networks?

That is not a niche question. It goes to the future of payments, treasury management, cross-border settlement, custody, financial supervision and monetary sovereignty.

Poland’s domestic context makes the silence even stranger

Poland is not a country where crypto is irrelevant.

A recent conservative estimate based on a CBOS survey commissioned by Dziennik Gazeta Prawna suggested that about 2 million adult Poles currently hold cryptocurrencies or related assets, with roughly PLN 40 billion (c. €10b) invested. Industry estimates are higher, though they should be treated with more caution.

Even the conservative numbers are enough to make crypto a mainstream household-finance issue, not a fringe hobby.

At the same time, Poland has spent recent months debating how to implement and enforce the EU’s Markets in Crypto-Assets Regulation. MiCA is already the central regulatory framework for cryptoassets in the European Union. Its stablecoin provisions have applied since June 2024, and the broader framework, including cryptoasset service providers, has applied since December 2024, subject to national transitional arrangements.

Poland has also been dealing with the consequences of a major crypto-exchange scandal involving Zondacrypto. Prosecutors have investigated suspected fraud and money laundering, with reported losses of at least PLN 350 million and thousands of affected clients. Whether the final losses prove higher is for investigators and courts to establish, but the case has already been large enough to become a public-policy issue.

In other words, crypto is not absent from Poland. It is absent from the mainstream financial conversation.

That is a very different diagnosis.

The Polish success trap

Polish banking modernised early and successfully. That is a strength. But it can also become a cognitive trap.

If a country has good banking apps, fast transfers and a successful domestic payment scheme, its financial elites may conclude that the future of finance will simply be an extension of what banks already do well. In such a mental model, digital finance becomes a banking upgrade. AI becomes bank efficiency. Regulation becomes bank stability. Programmable money becomes a question of whether banks can defend their role against non-bank players.

But blockchain-based finance is not merely a new front end for banks.

It changes the institutional structure of financial intermediation. It separates custody from brokerage, settlement from messaging, wallets from accounts, and programmable ownership from traditional record-keeping. It creates new risks, but also new forms of competition. It forces regulators to supervise entities, protocols, reserve structures, governance mechanisms and cross-border liquidity flows that do not fit easily into the traditional banking perimeter.

A financial congress that treats these questions as a one-hour side topic is not simply underweighting crypto. It is underweighting the institutional transformation of finance.

What this means for banks

Banks should not ignore digital assets because they dislike the speculative culture around crypto. The speculative layer is real, but it is not the whole story.

Stablecoins, tokenised deposits and blockchain settlement are already forcing banks to think about the future of money, liquidity and client relationships. If payment activity moves into wallet-based ecosystems, banks may lose not only transaction revenue but also data, customer interface and part of their role in working-capital flows.

This does not mean banks will disappear. That is not the point. The more realistic question is whether banks will become infrastructure builders in digital finance or whether they will defend their existing model until others build the rails.

What this means for regulators

For regulators, the problem is even more delicate.

Ignoring crypto does not make it safer. Treating it as a reputationally inconvenient topic does not reduce consumer risk. Refusing to engage with the sector does not prevent people from investing, using offshore exchanges, holding stablecoins or entering DeFi protocols.

Good supervision requires contact with the market. Not capture. Not promotion. Contact.

A regulator cannot supervise a sector well if its main posture toward that sector is distance. This is particularly important under MiCA, where national authorities will play a major role in licensing, supervising and enforcing rules for cryptoasset service providers.

The question is not whether regulators should be “pro-crypto”. They should not. The question is whether they can become competent enough to supervise the sector without pretending that it remains peripheral.

What this means for Poland

For Poland, the issue is strategic.

The country can remain a strong bank-technology market with limited influence over the next generation of financial infrastructure. Or it can start building competence in tokenisation, digital custody, compliant stablecoins, supervisory technology, on-chain analytics and capital-market infrastructure.

The first option is safer in the short term. The second is more demanding, but it is the one that gives a country a chance to participate in shaping the future rather than merely importing it.

This is why the imbalance in the EKF programme matters. It is not about event politics. It is not about whether one conference invited the right people. It is about what the Polish financial mainstream still considers worthy of serious discussion.

A one-hour discussion about programmable money, framed mainly as a challenge for banks, is not enough.

A broader conversation

One week after the European Financial Congress, Warsaw will host the 13th Digital Money & Blockchain Forum at Lazarski University.

The topic of the 2026 edition is Poland and MiCA: different approaches to digital-asset regulation, and who will win or lose under the emerging framework.

The Forum will take place on 8–9 June 2026 in Warsaw.

Registration and programme: https://digitalmoneyforum.biz/

The invitation is open to regulators, banks, fintechs, cryptoasset service providers, lawyers, academics, investors and anyone interested in the future of digital finance.

The central question is not whether banks will “lose ground”. The more important question is whether Poland wants to understand, regulate and build the next layer of financial infrastructure — or merely watch it emerge elsewhere.

Isn't it a typical case for a peripheral, dependent market organization. Outside of eurozone and with sovereign currency, it's hard to see strategies that go beyond strong, defensive ring-fencing. Over the last 20 years, resilient and relatively client-friendly banking (at least on the UX level) created a very comfortable position for the sector to thrive (it really stands out in Europe), and petrified into some sort of high stakes class, with merry-go-round between boards, regulatory and

government. Digital finance will arrive as adoption and cascading, with all types of opportunities missed.